Despite a lot of strong evidence suggesting that marijuana is at least as effective as prescription medication for a number of ailments, life insurance companies punish people who use this natural remedy. Even though marijuana use is extremely ubiquitous in modern America, the companies use archaic underwriting techniques for users of marijuana, making it unaffordable for many people. The way insurance companies classify anyone who uses marijuana, by smoking it or by ingesting with other methods, is to give them a risk rating of “smoker”, which normally is reserved for a tobacco smoker’s life insurance policy.

The problem is that tobacco use has been proven to be very dangerous to people’s health, while there is a lot of evidence that some marijuana can actually be beneficial for people. Because tobacco is so dangerous, it rightfully makes the cost of insurance much higher for users. When insurance companies give the same price to marijuana users they are preventing people from affording protection for their families, or they at least create an unfair financial burden for people who do purchase it.

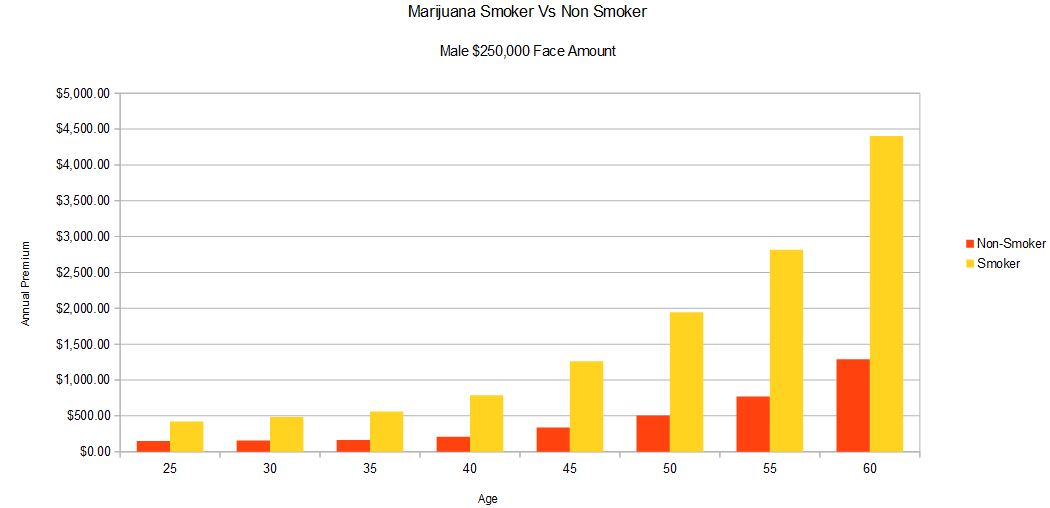

Considerably More Expensive

For a 35-year-old male who is otherwise healthy but smokes tobacco, the price of a $250,000 term life insurance policy becomes 3.5 times more expensive than a non-smoker.¹ This increase in price is such a burden that it means most marijuana users are under-insured, or even not insured at all. This pricing scheme is really hurting the beneficiaries (families) the most as marijuana user’s families are usually left lacking the protection they may need for their basic living if something were to happen.

This chart and table of data shows how prices compare for a healthy male smoker compared with a non-smoker of varying age for $250,000 of face value. These are actual premium costs of the least expensive term policy from all major companies for both smokers and non-smokers.

The cost of coverage is considerably less affordable as the insured person’s initial age progresses, however even for young people the cost of coverage is significantly more for the smokers than for those who don’t smoke.

Evidence Does Not Support The Cost

While a plethora of research exists linking tobacco smoking with statistically shorter lifespans, scientific evidence suggests that marijuana smokers are not more likely to get cancer², or die sooner³ than non-smokers according to studies.

Marijuana is also used to treat a number of diseases including diabetes, chronic pain, hepatitis C, effects of chemotherapy, fibromyalgia and many others. In most cases, a life insurance company will reward clients who routinely take their prescription drugs to control sickness and disease but this is not the case with marijuana.

With such clear evidence showing the medical benefit of marijuana for the treatment of specific diseases, coupled with the clear trend towards broad legalization, and the quickly growing amounts of users, it is far past time that life insurance companies update the way they classify (and price) clients who use marijuana in order to reflect what we know today about the plant.

This Can Be Fixed

As an example of a substance with proven deleterious effects being priced accurately look no further than alcohol. Social and recreational users of alcohol are not classified (for pricing) the same as someone who is an alcoholic. In fact, someone who drinks small quantities regularly can still qualify for the highest possible rates with the lowest costs. Why then does someone who uses small amounts of marijuana regularly pay such a significant price difference, when the health and mortality statistics do not corroborate the need for such high prices?

Effectively this is unfair discrimination against a large (and growing) portion of the American population. With the growing trend towards legalization, not only will there likely be more recreational smokers, but more of the current smokers will also be honest about their usage. This is going to lead to a bigger and bigger challenge for American families who are trying to be fiscally responsible by protecting their families with life insurance.

What we are asking is that the life insurance companies simply “get with the times” and update the way they price their life insurance. They must more accurately reflect the fact that marijuana poses (at most) minimal mortality risk and that to assign a tobacco smoker’s rating and price schedule to a marijuana user is unfair to users and to their loved ones. Simply speaking the current way of doing business is not fair.

*Editors Note: Life Ant does not recommend marijuana usage for recreational purposes nor are we recommending usage for treatment of any medical condition. We are not medical doctors and take no stance on legalization. We simply support fair pricing of life insurance for everyone, and our CEO takes great pains to reduce the cost of life insurance for all his clients including those who use marijuana, both medically and for recreational reasons.

1.Quotes from LifeAnt.com

2.http://www.ncbi.nlm.nih.gov/pubmed/9328194

3.http://www.ncbi.nlm.nih.gov/pmc/articles/PMC1380837/