A 401(k) is an extremely important tool for retirement and for personal savings. A 401(k) is important because it represents (by far) the biggest source of retirement funds outside of Social Security, and for many people, it is the easiest way to put money away regularly.

Most workplaces offer a 401k plan, but too many people don’t take advantage of the offering. This is not very smart. If you have the option of enrolling in a 401(k) plan through your work, you need to sign up today! Signing up and enrolling is extremely easy, and we will walk you through everything you need to know to get started.

What is a 401(k)

A 401(k) is a retirement savings account offered through work. It allows employees to elect to contribute a portion of their wages from every paycheck into a tax-qualified investment account. 401(k) plans are recognized by the IRS as a way to legally defer salary into a retirement account pre-tax, and they are the most common investment accounts that American’s own. Every pay period a percentage of your pay can be sent to the 401(k) plan and allocated into various investments, which grow completely tax-deferred until the money is withdrawn.

The caveat is that your money can not be withdrawn until you reach at 59.5. If you withdraw the money before you turn 59 and a half, you may need to pay a 10% federal tax penalty in addition to the regular taxes, except by taking or loan or from provisions allowed by hardship exemptions.

Why You Need to Enroll

You need to enroll for three very important reasons. The first is that you need the money for retirement, the second is that you are incentivized to do it through the tax code, and the third and most important reason is that if your company offers a match, you have the opportunity to give yourself free money!

Most companies offer what is called a “match”, meaning that they will add matching money for every dollar you put into your 401(k) plan up to a certain amount. Typically, a company will offer a matching scheme such as a dollar for dollar match up to 3%, or a 50% match up to 5%. Companies do have the freedom and discretion to choose how, and if, they provide matching money for their employee salary deferral. Whatever they provide, you need to take advantage of this very powerful feature to give yourself free money. It’s like giving yourself a raise.

Keep in mind that whatever money you defer from your salary, it will come out of your paycheck tax-free. So if your money is taxed at 30% and you put in $1, it actually only reduces your net pay by $ .70. You may not really notice much of a difference in your actual check, despite the fact that you are putting away a significant amount of money. The money is taxed when it is withdrawn from the account.

As we said before, beware! If you need to take money out of your 401(k) before age 59.5, you will be subject to a 10% tax penalty, on top of any federal tax you already owe. Each state also has individual tax rates for withdrawals.

Where to Start

You need to fill out the enrollment paperwork to begin contributing to a company-sponsored 401(k) plan. The enrollment paperwork is typically a packet that includes forms for your financial advisor, third party administrator, and payroll company. It can ask you some questions about how you want to divide the money up within the plan as well. Read below for additional help with these sections.

If your company is big enough they probably have a human resources department. It is the job of the human resources department to know everything about enrolling in the 401(k) plan, though it is illegal for anyone from human resources to give you investment advice. If you don’t have a human resources department, your company should have someone in charge of the plan, or at least an investment advisor who can help you get set up with the plan.

The setup also needs to also be coordinated with the payroll company, so make sure that whoever is in charge of payroll at your company is notified that you are enrolling in the plan so that they can deduct the appropriate amounts from your pay to be invested in the plan.

If no one at your company knows how to help, you can call the third party administrator (TPA) of the plan. If your company offers a 401(k) plan, they definitely have a TPA because it is legally required for record-keeping purposes. If your company offers a different type of plan such as a Simple IRA, they may not have a TPA. The TPA will be able to provide enrollment paperwork and literature on investment offerings. If you do not have a TPA, the investment advisor will be your contact.

Enrolling in the Plan

When you fill out the enrollment paperwork, you are going to be asked to make some decisions. The first big decision is how much of your paycheck you want to put into the plan. So that you understand the lingo, typically it will be phrased as a question about the “percentage of salary deferral”.

How Much to Save

Here is the simple rule. You want to save at least enough to get the maximum amount of matching money from your company that you can. So if your company offers a 100% match up to 4% of your salary, you need to save at least 4%. If your company offers a 50% match up to 6%, you need to save at least 6% of your salary. This is as close as it gets to “free money”, and you want to take advantage of any money that your company is willing to give you.

If you are behind on your retirement savings, you might need to save more than the maximum amount your company will match. You should consult a financial advisor if you are unsure where you stand. They will be able to conduct a financial analysis predicting the future growth of your savings and compare it to the amount of time you have left before retirement, and how much you will need to survive on while you are retired. Many financial experts recommend that people save a minimum of 10% of their pay into their retirement accounts. This may seem high, but when you do the math you will probably realize that you need it.

Choosing your Investments

Your 401(k) probably has restricted investment options. You may have a single fund family, with something like 15 to 30 funds to choose from, or you may be able to choose between more funds if your plan is set up to do that. Typically a 401(k) is somewhat restrictive on investment options, which can be good for the average investor even if it does prevent them from investing in certain funds that they may want to invest in.

Find your Plan Advisor or Broker of Record

No matter what your realm of choices are in your 401(k), correctly allocating your money is the most important part that determines how much money you have when you retire, apart from choosing to sign up and contribute. Allocating your 401(k) is where things get confusing, so you may want to enlist the help of a professional investment advisor. Usually, your company can refer you to what is called “the broker of record” on the 401(k) plan, who can give you advice on how to invest your money in the plan. Be aware that there are different levels of “advisors” for 401(k) plans. Sometimes the advisor actually has what is known as a fiduciary duty, which obligates them to offer good investment advice to all the plan participants. Sometimes they are only a broker and don’t have a legal requirement to ensure that you are given appropriate advice.

What an Advisor Will Do For You

A good advisor will sit down and meet with you, and ask you to fill out a risk questionnaire. This is a very important piece of properly allocating your investments. It asks questions like what percentage of your total worth is in this retirement plan, how soon you need the money, when you are going to retire, how much risk are you willing to stomach, and how much money you are going to need at retirement. Balancing all of these factors, your advisor can recommend a suitable portfolio. If you feel like this is over your head, don’t worry because your advisor can explain. You will be wise to understand it though because it can make a big difference if the market drops. You need to understand what is normal when the market drops, and you need to understand when you are building your portfolio just how big a swing in value your account may see. Depending upon which investments you choose, the swings in value can be very huge or very small with market fluctuations.

After your advisor determines the results of your needs and appetite for risk, she will recommend funds in a suitable mix between stocks and bonds, and possibly other asset classes like commodities (held in the form of a mutual fund). A conservative allocation might be 100% bonds. An aggressive allocation might be 100% stocks. Theoretically the higher percentage of stocks, the greater your expected return is over the long term, but the bigger the swings in value as the market goes up and down. An advisor will not only help you understand this but also will choose a mix of funds that balances growth with volatility. For instance, a mutual fund made up of all small-cap funds (small companies) will show a long term growth rate that is big, but will probably go down more than the overall market in bad times. A large-cap dividend fund made up of blue-chip companies will not grow as much as the overall market during boom times, but it will also throw off dividends and be less volatile during hard times. Bond funds have similar trade-offs, and actually, have even more complexity than stock funds.

Allocating Your Own Investments

If for some reason you do not want to use this broker, or he/she is unwilling or unable to provide good help, here is a basic guide on how to set up your allocations, with a couple of options.

Buy a Target Date Fund

Perhaps the easiest, and if you are overwhelmed by all of this then the smartest option is to buy a target-date fund. Pretty much every 401(k) plan offers them these days, and they are easy to use. All you do is choose the date that corresponds with your most likely retirement date. This is the only fund you buy, and as you get close to retirement the fund will automatically rebalance to become more conservative. You want your investments to be more conservative when you are closer to retirement because you don’t have time to hold through a market crash.

If you are going to be 70 in the year 2035, or close to it, allocate 100% to the 2035 target-date fund, and let the fund managers do the rest. You won’t need to think about any logistics along the way. Target date funds have become an excellent option for the average investor’s retirement portfolio.

Build an Intermediate Risk Portfolio

Another option, if you are a little more comfortable picking your own investments, is to build an intermediate risk portfolio comprised of stock and bond funds. You will want the overall mix to look something like 30% bonds and 70% equities (stock funds), but you can vary this a bit (between 25%/75% bonds to stocks and a 50%/50% mix) depending upon your comfort levels and appetite for risk. Keep in mind that the higher your percentage of equities, the higher the likelihood that you will experience bigger swings in your value due to market fluctuations. Bond funds are not immune to fluctuations (mostly from changes in interest rates) but generally, are more stable as a rule.

An intermediate-risk portfolio is optimal because it has a high enough percentage of equities so the owner can make a lot of money, but also enough invested in bonds so that the portfolio will be safer and experience less severe downturns when the market recedes. If you are younger and/or more aggressive, you can allocate a bit more to stocks. If you are nearing retirement or retired, or if you are generally more conservative, you can choose to put more money into bonds. Generally, and 70% stocks to a 30% bonds investment mix works for the widest group of people.

Within this 30/70 portfolio, we suggest that you do some research into the various funds. Try to split up the money between at least 3 stock funds and at least 2 bond funds. Don’t be afraid to split the money between 8 or 10 funds if you are comfortable doing this, but it is not necessary.

When you are setting up a 401(k) account, this setting up of the investment mix is called the contribution allocation. It is how every dollar that you put into your 401(k) will be broken up for purchasing the funds.

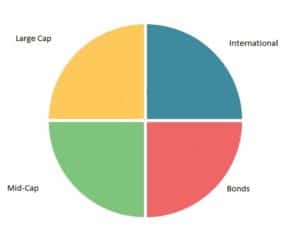

Types of Stock Funds

With the stocks, there are 3 classes that you may want to invest in and give yourself some exposure to. Your biggest stock investment should be a large-cap fund comprised of American equities, preferably one that pays dividends. If you are a bit more aggressive you can choose a growth fund, if you are more conservative you can choose a dividend fund or some mix of both.

In smaller amounts, you will want exposure to at least one international fund. International funds are important today because growth outside the United States is happening at a faster pace in many instances, and if US companies are going through a slow period, sometimes international companies are booming (though their fortunes are of course intertwined). Choosing assets that boom and bust in different cycles is another way of saying that they are not highly correlated. This can help minimize volatility in your portfolio.

The third type of equity fund that you will want some exposure to is a small or intermediate cap fund. This means that the fund primarily invests money in smaller to medium-sized businesses, as judged by the total value of the company (market capitalization rate). Small business can grow much faster than the biggest companies, and they can also be taken over. A takeover usually results in a big jump in the stock price, resulting in great returns for shareholders. The downside to smaller companies is that they are more prone to fail, especially in bad economic times. Choose these types of funds with caution.

A good mix of equity fund distribution is to be 60% large-cap funds, and 20% each international and small/medium cap funds. You can also substitute in very small amounts some other types of funds such as mineral funds, real estate funds, or other specialty funds.

Rebalancing

Stock and bond prices move every day that the markets are open. As a result of this daily fluctuation, your investment mix will also change. Stock gains normally outpace bond gains. After a few months or a year, you may notice that your portfolio is now 75% stocks instead of the original 70%, as the value of stocks grows quickly. The way to combat this effect, and to keep your investment mix to relatively stable, you need to set up automatic rebalancing.

Rebalancing is the act of making trades in your portfolio in order to return it to the desired proportion of each investment. If your portfolio has 5% too much money invested into stocks, rebalancing will move 5% of the total money out of the stock funds and into the bond funds proportionally, until the desired percentage of your total value that you choose for each individual fund is attained.

It may sound complicated to calculate how many shares should be traded out of and into each investment, but it is easier than you think. Every brokerage has built calculators to figure the trades out automatically. All you need to do is to press the rebalance button, or ideally to set it up to run automatically.

You can choose whatever frequency that you would like for rebalancing, typically monthly, quarterly, semi-annually, and annually are the options. We recommend that you choose semi-annually or annually. This is because it gives enough time to capture more of the gains if certain funds are outpacing the others, but a short enough window to give a good chance of locking in those gains.

Benefits of the 401(k)

Getting set up for regular contributions to your 401(k) plan is an excellent idea. It is a great way to save money for retirement, and it also has a lot of other handy uses. Some of these great benefits are:

- Having an Emergency Fund

- Showing assets to a lender if you are applying for a loan

- Saving your money pre-tax

- Practicing Saving

- Getting a matching contribution from your employer

- Having an account to loan yourself money from

We highly encourage everyone to get themselves set up and contributing to a 401(k) plan.