Modified coverage is a less expensive form of life insurance which is unlike a traditional coverage life insurance policy because the death benefit changes over time. Typically, the amount of coverage will decrease over time, which corresponds to a reducing need for coverage. An example would be mortgage insurance, where the death benefit will drop and will always generally correspond with the remaining principal of the mortgage. The advantage of modified coverage is the lower cost of insurance for the policy owner. The premium payments are level throughout, so the owner can enjoy lower premiums even in the highest coverage years of the policy!

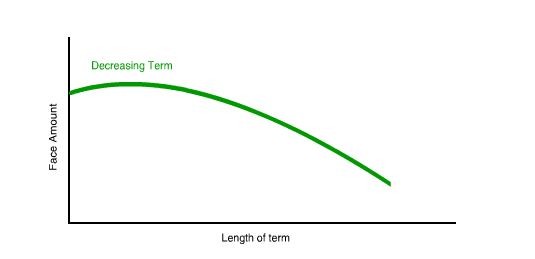

Modified coverage does not only have to be decreasing. Increasing whole life and term policies can both be purchased. Decreasing term life insurance is perhaps the most common form of modified coverage. To illustrate how this works, here is a graph showing insurance coverage over time with a decreasing term life policy. The premium payments are always level.

Purpose

Modified coverage policies are useful for owners in a number of different situations. Decreasing coverage policies are useful as mortgage insurance, education expense insurance, retirement savings insurance, and to accommodate the decreasing amount of coverage needed to provide for a child as they get older and closer to providing for their own needs.The purpose of modified coverage is to provide both the needed protection and to ensure future insurability for the insured person without paying for more coverage than the owner has to.

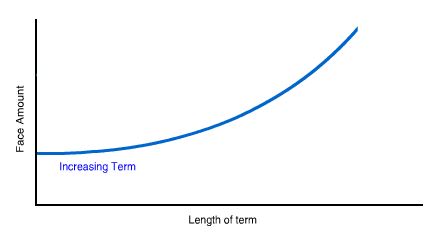

Increasing coverage policies are useful for younger people who will need more income protection as they make more money, families who will be having and caring for additional children in the future, or a business buy-sell agreement between partners where the business value will appreciate and higher levels of life insurance will be needed to compensate the deceased family for their share in the business. Of course an increasing coverage policy will cost more than a decreasing coverage policy which starts at the same death benefit level, but an increasing coverage policy may be less expensive than adding additional insurance coverage later in life. Increasing term coverage looks like this over time:

Mortgage Life Insurance

Mortgage life insurance is perhaps the most common use for modified coverage policies. This is usually structured as a decreasing term insurance policy, where the value of the death benefit of the policy generally corresponds with the remaining principal left on the mortgage. This is a less expensive way to provide protection against mortgage payments after an income member earning of a family passes away than simply purchasing a level term policy for the value of the mortgage.

Many people only purchase mortgage life insurance if they can not afford more coverage, as this is often the most useful obligation that they can eliminate for their family after they pass away.

Retirement Insurance

A certain amount of savings must be put away for someone to retire comfortably, and as people get older they generally get closer to this savings goal. A common use for decreasing coverage is to make up this shortfall, which should lessen with age. This will allow the surviving spouse to retire comfortably, without the income power of the dead spouse. Term policies that end during an insured person’s younger years also tend to be less expensive than those that end later in life.

Education or Dependent Needs Support

Providing for the needs of a child, education included, is often a priority of people who own life insurance. The total amount of coverage needed to pay for this support will usually decrease with time though, because the child is older and closer to providing for themselves, and a parent often has saved more money towards a college education as the child gets closer to this age. A modified coverage decreasing face value policy may be useful for someone who doesn’t need the extra coverage, or for someone who would like to save money while still providing for their child’s needs.

Preparing For Higher Earnings

A reason someone may purchase a policy with an increasing face amount is because they expect their income to increase in the future. With an increase of income, most people can expect that their lifestyle and families monetary needs will also increase. By purchasing a policy that either gives the owner the option to buy additional insurance at regular intervals, or by purchasing an increasing term life insurance policy, the insured person will know that their income can be replaced if they were to pass away prematurely.

Decreasing Coverage Provides Best Savings

Decreasing coverage is very popular among people who want to save money on their life insurance. While still providing the needed protection, there is not any money wasted as the need for coverage diminishes. This level premium structured product has lower premiums than a level coverage policy of the same amount. To see how affordable a modified coverage policy can be for yourself simply start by entering your zip code in the quote tool above.

At Life Ant we recommend that our clients who do not want to commit large amounts of their financial resources to life insurance examine quotes for decreasing coverage policies because this may provide such substantial savings over time.