Mortgage life insurance is a term life insurance policy meant to pay off a mortgage should one or both parties responsible for the mortgage perish. The death benefit on mortgage life insurance will decrease over time, with the face value always being approximately equal to the payoff amount of the mortgage. The decreasing death benefit means that mortgage life insurance is less expensive than a level term policy, all else being equal.

Because a mortgage is often the most burdensome bill that a spouse or family will be left with if an income earning member passes away, mortgage life insurance represents an important minimum amount of life insurance coverage that most families should hold.

How Does Mortgage Life Insurance Work?

Mortgage life insurance is a term life insurance policy, which lasts for as long as the length of time that payments are due on the mortgage. Usually companies will sell the coverage in 15 or 30 year increments, which match the most common lengths of mortgages taken out by consumers of bank mortgages.

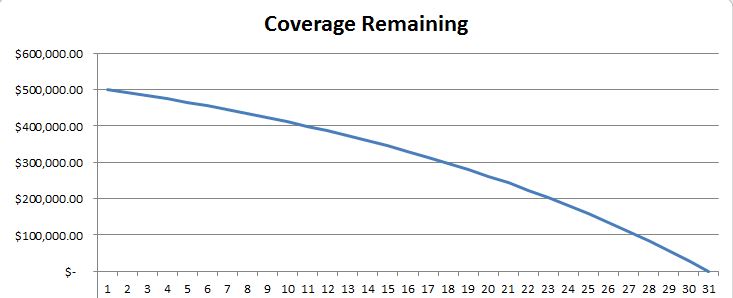

The coverage decreases over time, always approximately corresponding with the amount of debt left to pay off the full mortgage amount. Practically speaking, the face value would look about like this for a 30 year $500,000 mortgage:

You can see how the face value drops over time, in line with the amount of payoff left on the mortgage. After the amount of time passes where the mortgage is supposed to be paid off, there is no face value left on the policy. Some companies may set minimum levels that the face value can drop to before it reaches 0, usually about 20% of the face value. After the term of the policy expires however, there will no longer remain any coverage.

Why Use Mortgage Life Insurance?

People use mortgage life insurance to lessen the largest burden on their families if they die, which is usually the mortgage payment. This allows the remaining family members to pay off the mortgage, own the residence outright, and no longer have any monthly housing costs.

When comparing the price of mortgage life insurance to a level term policy, the mortgage life insurance coverage costs less money in premium payments than the level term. This is because the face value drops over time, unlike the level term which stays the same for the entire time the policy is in force. For this reason mortgage insurance presents an affordable way for income earning members of a family to erase what is usually the biggest source of debt for the survivors. Even if they choose to sell the house, the total proceeds can go towards purchasing a new residence, hypothetically debt free as long as the purchase price is lower than the proceeds from the sale.

Also because of the decreasing risk to the life insurance company over time as the policy ages, people who are not otherwise insurable for a traditional life insurance policy may still be able to obtain mortgage life insurance.

Mortgage Insurance Does Not Have To Pay A Mortgage

Perhaps some may consider it an oddity of life insurance laws that the owner has complete control over who the beneficiaries are of a policy, and the beneficiaries have complete control over what they do with the benefit that they receive. This is important to people who have taken out a mortgage life insurance policy because these rules mean that the death benefit does not necessarily need to be used to pay off a mortgage. The bank does not need to be named as a beneficiary, and the beneficiaries who receive the payment do not need to use the proceeds to pay off the bank. It is completely within their discretion to decide what to do with the money they receive.

Proof that a mortgage was loaned does need to be supplied by the prospective policy owner to receive mortgage life insurance, and the life insurance company will calculate the amortization of the loan so the policy death benefit will always roughly coincide with the amount remaining, but any claims are treated just like any other form of life insurance.

Changes to the Mortgage Do Not Affect The Life Insurance Coverage

If a mortgage is paid off sooner, or extended, it does not change the timing of the face decreases of the life insurance policy. Once the policy is issued, it will remain exactly as originally written regardless of how the remaining mortgage balance may deviate from initial expectations. It does not matter what occurs with the mortgage, or even if the mortgage still exists, the policy will provide coverage based on the initial schedule.

It should be noted that other forms of decreasing face life insurance do exist. This may also be referred to as modified face or modified coverage life insurance. The timing and amount of the face decreases may differ significantly from mortgage life insurance, but the cost savings benefits remain over level face policies.

Mortgage Life Insurance Is a Useful Minimum Coverage Amount

People use mortgage life insurance because it is cheaper than level coverage policies, and the coverage provides a very useful benefit by paying off the remaining mortgage. If the breadwinner of a family passes away, most spouses who remain and other remaining family members can often earn enough money to provide for the family without sacrificing their currently lifestyle, if the mortgage is paid off. This is why many people find mortgage life insurance to be an extremely cost effective and useful policy to own.

To receive quotes for mortgage life insurance please use our quote tool above, and feel free to visit our life insurance quotes page as well.